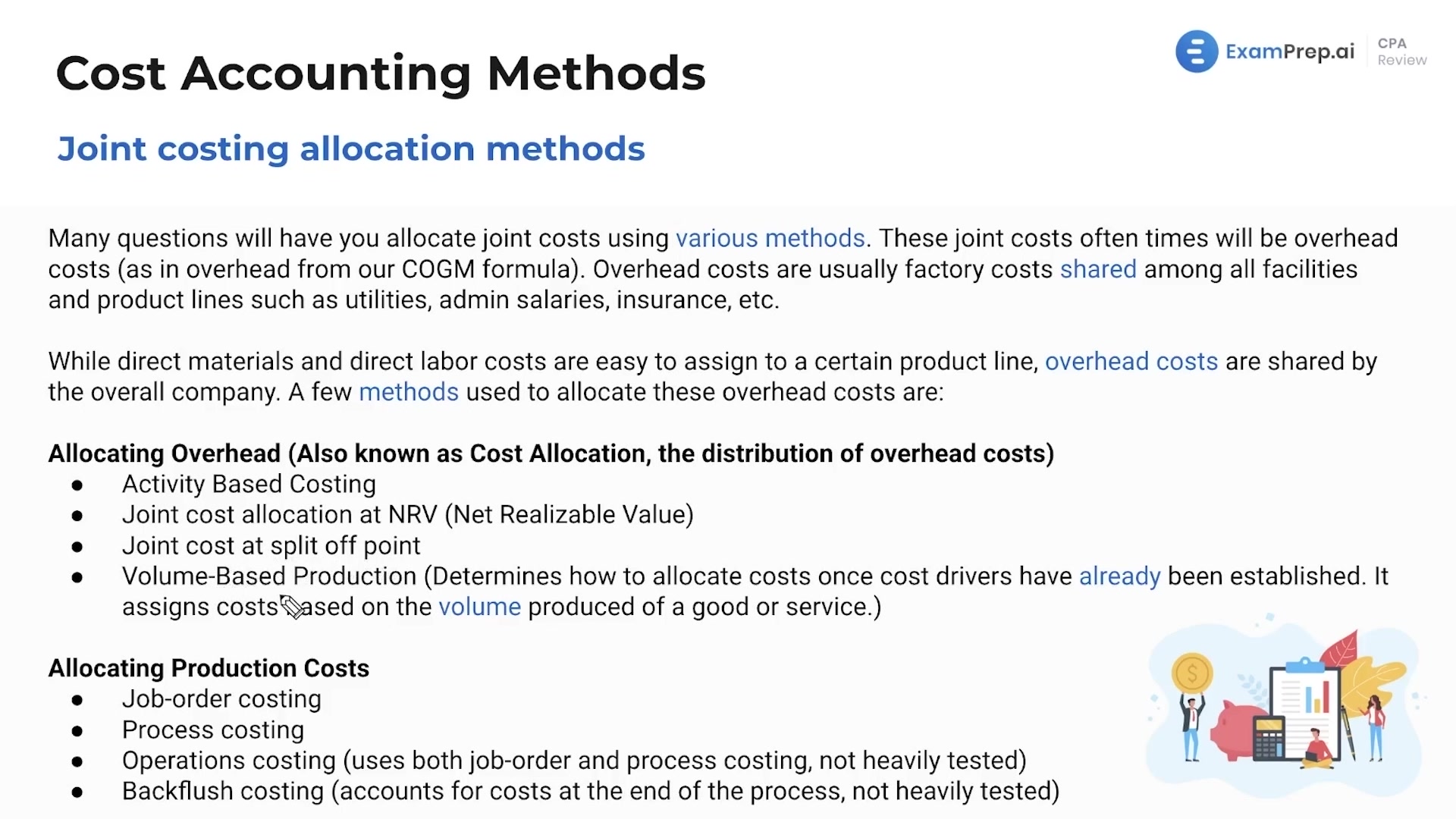

Work in Process vs Work in Progress: What’s the Difference?

Depending on the scope of the undertaking, they may be better suited to report work in process or work in progress. In both cases, a company develops an asset but the reporting and accounting treatment may vary. Work in process is an asset account used to report inventory items not yet completed.

Work In Process vs Work In Progress: What’s the Difference?

A work in process means that you have products that move from raw materials to a finished product within a short period of time. They may be called goods-in-process and include manufactured goods that the production team completes in less than a full work in progress or work in process accounting cycle. However, the nature of each may be slightly different and require different accounting treatment. Work in process may refer to items of inventory with quicker turnover. The terms “work in progress” and “work in process” are used interchangeably to refer to products midway through the manufacturing or assembly process. Developers and manufacturers take raw materials and convert them into finished goods.

Writing Topics

We’ll go over that in detail in this article, plus teach you how to use the correct phrase in a sentence. On the other hand, work in progress is more representative of massive, one-time undertakings. These projects have much longer timelines and may take years to complete a single instance.

The Construction-in-Progress Account

A work in progress is a project that is not yet finished or polished. One might say this about a work assignment, a home renovation, or about one’s relationship with another person. If you ever get stuck, feel free to come back for a quick refresher. We’ve got a whole library of content dedicated to explaining confusing words and phrases in the English language. The distinction between “In Process” and “In Progress” offers a more nuanced approach to task management and communication.

- In summary, a work in progress for business purposes is a project that is on the way to completion.

- One might say this about a work assignment, a home renovation, or about one’s relationship with another person.

- However, they have different meanings, so doing that could cause the meaning of your writing to be lost.

- Some people use these phrases interchangeably, but there are differences between the phrases you should be aware of.

A company has started taking raw materials and converting them to a finished product to sell. However, that final product is not yet done and is not yet ready for sale. Work in process is usually used to report manufactured, standardized goods. This time frame represents how long it takes for a product to be finished.

In a bind, a company will find it much easier to liquidate work in process items. Though these goods are incomplete and still require some work to become finalized goods, the time span in doing so is much shorter than work in progress goods. In addition, the market may be more willing to buy work in process goods outright if they are for standardized goods. Manufacturer of commercial vehicles Charisma Motors is known for producing sedans, cross-overs, and SUVs. In the manufacturing facility, vehicles move along an assembly line and pass through various work stations. Engineers and machines install and secure new parts at each stage.

Work in progress has always been preferred in British English. Work in process was more popular for a short period in the 20th century in American English, although today work in progress is again the preferred term. Whether you are selling a product, offering a service, or working on a project to develop your business, you will need to be attuned to the relevant WIP values. And now that you know the distinction between work in process vs work in progress, you will be prepared to efficiently inventory these different values.

Definition of ‘Work in Process’: What Does ‘Work in Process’ Mean?

Since every business will have both works in process and works in progress (both of which can have the acronym WIP), it is clear that you must learn how to calculate their values. Read on for an overview of the meaning of work in process vs work in progress. No subscription fees and rates up to 50% cheaper than other online editing services. AI is a great tool, but when it comes to perfecting your writing, we rely on real human editors.

In accounting, both phrases refer to the cost of unfinished goods for a business. They might create work-in-progress reports to let the boss know the financial status of their current projects. Every product goes through a manufacturing process that converts it from raw materials to a completed item that a company sells. Custom doorknobs, wrought iron railing, and other iron and steel fixtures are made for homes by Branson Metalworks. Branson Metalworks discovers that they frequently have about 200 orders completed and about 35 orders still in the manufacturing process at the end of each quarter. Any ongoing work is counted as work in process when calculating its assets.

The project would take about two years, Carrot Computers discovered after working with its point of contact. The definition of ‘in process’ works in any of the stages it goes through to get to the finished product. The phrases are used to describe work or a task that’s not completed yet but is currently on the way to completion. For instance, a large-scale project might have certain stages that remain “In Process” for extended periods due to the depth and intensity of work required. “In Progress” is a broader term that encompasses any task or project that has started but is not yet complete.

It has the same meaning, and can be used in all of the same contexts. For many of us, writing is a skill that we are continuously building. Even when we feel accomplished, we are always working to become even better. We might say that our development as writers is always in progress.

It’s a small yet powerful distinction that can make a significant impact on how we organize and execute our work. While both terms describe tasks that are not yet complete, their nuances can significantly impact how we perceive and manage our workflows. For instance, in software development, a feature might be “In Process” when it’s in the coding phase, with developers actively writing lines of code to bring the feature to life. Similarly, in manufacturing, a product might be “In Process” as it moves through various assembly lines, undergoing different treatments and transformations.

- That project might be a service you sell, meaning you must record its value, even while in progress.

- While both terms describe tasks that are not yet complete, their nuances can significantly impact how we perceive and manage our workflows.

- Some writers aren’t sure whether to use work in progress or work in process, but you will discover the truth in this article.

- The project would take about two years, Carrot Computers discovered after working with its point of contact.

What are the benefits of using “In Progress” in project management?

Shortening it to in-progress carries the same meaning as is much easier for the reader. According to Merriam-Webster, the phrase ‘in progress’ means a project that’s not finished yet. Now that you know there’s no real difference between the phrases (other than the preference of use), let’s look at what they mean in more depth. No matter what side of the Atlantic you are writing, the phrase you are searching for in the 21st century is work in progress.